News

19 Mar 2026, 13:25

YBTC: Bitcoin Covered Call Strategy May Outperform Bitcoin, But Risks A Market Correction

Summary Roundhill Bitcoin Covered Call Strategy ETF (YBTC) is rated Sell due to downside risk from bitcoin’s corrective wave, despite potential near-term outperformance versus bitcoin. YBTC employs a synthetic covered call strategy, offering high yield (76.31%) but exposes investors to full downside risk and NAV erosion. Recent bitcoin ETF fund flows may have normalized the market environment, potentially stabilizing bitcoin volatility that can benefit YBTC’s income strategy. YBTC’s distributions are 100% return of capital, providing tax deferral but increasing risk of capital erosion over time. YBTC SA Repot 3.18.26 The Roundhill Bitcoin Covered Call Strategy ETF ( YBTC ) is an alternative income exchange-traded fund designed to provide investors with indirect exposure to bitcoin through a synthetic covered call strategy. While covered call strategies tend to limit the full upside potential of the fund given the short call position, the market may be positioned for YBTC to outperform bitcoin, creating a differentiated investment opportunity for those seeking exposure to the performance of bitcoin while earning income through a derivatives strategy. While I believe YBTC may outperform bitcoin in the near future as a result of the premium earned on sold call options, bitcoin may be entering the final corrective wave when applying Elliott Wave Theory, suggesting that the price of bitcoin may continue its decline going forward. As a result of this, I am recommending YBTC with a Sell rating. Investment Thesis for YBTC YBTC employs a synthetic covered call strategy to provide investors with exposure to the performance of bitcoin. A synthetic covered call strategy is similar to a covered call strategy with respect to taking both a long and short position with respect to the underlying asset; the core difference between the two types of strategies is that a synthetic covered call strategy is entirely made up of derivatives whereas a covered call strategy has direct ownership of the underlying assets. In the case of YBTC, the fund provides indirect exposure to bitcoin by taking both long and short positions in options derivatives, though has the flexibility to take a direct position in a bitcoin ETF per the fund’s prospectus . The fund does this by buying call options and selling put options to create synthetic long exposure to bitcoin. In turn, the fund will sell out-of-the-money call options in order to earn premium for the fund. While this can be an appealing investment strategy when the price of bitcoin trades within a certain range during the options’ holding period, the fund may limit the full upside potential as a result of the covered call options sold while exposing investors to the full downside risk during a market correction. On the basis of these factors, I have reason to believe YBTC could outperform bitcoin in the near future following a series of repositionings that occurred in late-2025 and early-2026. Towards the end of 2025 , bitcoin underwent a major correction that led to the liquidation of over $19b in leveraged positions within a 24-hour period. These events were the precursor to a further price correction with bitcoin declining to a 1-year+ low of $62.1k per coin in February 2025 before modestly recovering. TradingView (TradingView) While I believe the liquidation of leveraged positions was the beginning of the price correction, I suspect a large component of the deeper decline was the result of the institutionalization of bitcoin, adding bitcoin exposure through the use of spot ETFs in portfolios of individual investors that may not be as comfortable with the volatility bitcoin presents with respect to traditional equity and fixed income funds. Bitcoin spot ETFs were established in January 2024 following the approval by the SEC , leading to billions of fund inflows into these bitcoin spot ETFs. With the emergence of these funds came the emergence of risk-averse investors seeking to participate in the returns of a risky asset. Bitcoin ETF AUM (Bitcoin ETF Fund Flows) In addition to this, with the mass adoption of bitcoin ETFs, liquidity was fundamentally baked into the ETFs, providing investors with a highly liquid asset that can be converted into cash with minimal spread risk . I suspect that the initial price decline experienced in October 2025 led to the widespread exodus from bitcoin spot ETFs and potentially the repositioning out of less liquid funds and into funds with greater assets under management. Bitcoin ETF flows (CoinGlass) You may recall that the market exhibited euphoria in 2025 with the passage of the GENIUS Act and a number of other legislation being considered to provide safeguards for cryptocurrency as well as the establishment of the strategic bitcoin reserve . Despite the political support for cryptocurrencies, the market remains as the ultimate price-setting mechanism for the coins, determining the price of bitcoin based solely on supply and demand. Looking ahead, I believe bitcoin exposure has been in a state of normalization following said period of euphoria. While the price decline may continue in the future, or reverse, I suspect that the steps laid out above, inclusive of the liquidation of highly leveraged accounts and ETF fund outflows, are suggestive that the greater risk to price volatility has been reduced. This could eventually result in price stability, providing an ideal environment for YBTC to perform its best. Looking at the technical chart, I have reason to believe that the price decline of bitcoin is entering the final wave down in the retracement cycle when applying Elliott Wave Theory. Elliott Wave Theory is based on the Fibonacci Sequence, measuring the market through a wave pattern with 5 wave cycles up followed by 3 wave cycles down. This may mean that the final corrective wave is imminent. Elliott wave chart (TradingView) The completion of the final downcycle may result in a reversal or a continuation of the downcycle, which may be dependent on investor sentiment and potential exogenous factors that may occur in the future. Given the potential for the 3rd downcycle, I believe YBTC may face downward pressure, though it has the potential to outperform bitcoin on a total return basis. While the fund exhibits full downside exposure through the synthetic long position, YBTC will continue to earn premium from the sale of out-of-the-money call options, generating incremental value. About Roundhill Bitcoin Covered Call Strategy ETF YBTC was launched by Roundhill on January 18, 2024 on the Cboe BZX Exchange. The strategy has a gross expense ratio of 96bps, a relatively high fee when compared to peer bitcoin covered call strategies. ETF comparison table (Seeking Alpha) YBTC has roughly $171mm in net assets with an average of $4.33mm in share value changing hands on a daily basis, providing moderate liquidity for investors seeking to trade the fund. YBTC pays out weekly distributions with an annualized rate of $17.66/share over the last twelve months, yielding 76.31%. Dividend history (Seeking Alpha) When evaluating these types of funds, investors should review both total returns and price returns to fully understand the value earned from ownership. Per the fund’s most recent 19a-1 notice, 100% of the distribution was derived from return of capital. ROC provides investors with a tax-deferred benefit that lowers the cost basis of the investment. Once the cost basis reaches $0/share, excess ROC will be taxed as capital gains. The benefit of the fund’s price decline is that the future price at which the fund may be sold can potentially narrow the gap, though will also influence the actual return the investor earns from owning the fund. As part of this, investors will be faced with NAV erosion that may deteriorate the value of their investment over time. Total return (TradingView) Price return (TradingView) Risks Related to YBTC YBTC provides investors with exposure to a synthetic covered call strategy, presenting certain risks that should be considered prior to making a final investment decision. Synthetic covered call strategies may limit the full upside potential for an investor while exposing them to the full downside risk of the holdings. The strategy is dependent on market liquidity and potential volatility to earn premium on options sold; greater volatility in the underlying asset may result in higher premium earned. Tighter liquidity in the options market that the fund participates in may result in uneven options pricing. As a result of the underlying strategy, investors may be exposed to NAV erosion over the course of their holding period. Investing in YBTC is not a direct investment in bitcoin. Final Thoughts With bitcoin undergoing a potential corrective wave, YBTC may be positioned to outperform bitcoin, though may face downside exposure resulting from its long bitcoin call and short bitcoin put options positions. As a result of this, I am recommending YBTC with a Sell rating.

19 Mar 2026, 13:25

Opera CELO Tokens: Strategic Pivot Sees Browser Giant Propose 160M Token Stake

BitcoinWorld Opera CELO Tokens: Strategic Pivot Sees Browser Giant Propose 160M Token Stake In a significant strategic shift, Nasdaq-listed browser developer Opera has formally proposed converting its existing cash-based partnership with the Celo Foundation into a substantial 160 million CELO token allocation. This pivotal move, if approved by Celo governance, would fundamentally alter the financial and operational relationship between the two entities, positioning Opera as a major stakeholder within the Celo ecosystem. The proposal marks a notable evolution from a service-for-cash model to a deeper, token-aligned partnership, reflecting broader trends in the convergence of traditional technology firms and decentralized networks. Opera CELO Tokens Proposal: From Cash Grants to Ecosystem Alignment Opera’s new proposal directly replaces a previous agreement established with the Celo Foundation. Under the original terms, the Foundation provided Opera with quarterly U.S. dollar-denominated grants. In exchange, Opera committed to expanding the Celo ecosystem through integration and promotion within its widely used MiniPay wallet . This stablecoin-focused wallet, built directly into the Opera browser for users in key markets like Africa, served as a critical user onboarding tool for Celo’s financial applications. The revised agreement would terminate these cash payments. Instead, Opera would receive an allocation of 160 million native CELO tokens, distributed over a three-year vesting schedule. This shift represents a strategic bet by Opera on the long-term value and utility of the Celo network itself, rather than simply acting as a paid service provider. Consequently, the company transitions from an external contractor to an internal stakeholder with a vested interest in the network’s success. Analyzing the Scale and Impact of the Token Allocation The sheer size of the proposed token allocation underscores the transformative nature of this deal. Based on current circulating and total supply metrics, the 160 million CELO tokens would represent a substantial portion of the network. Circulating Supply Stake: Approximately 27% of the current circulating supply of CELO. Maximum Supply Stake: Roughly 16% of the token’s maximum supply cap. This scale immediately positions Opera as one of the largest single entities within the Celo ecosystem. However, the proposal includes a critical governance limitation to maintain network decentralization. Despite the potential size of its holding, Opera’s voting power in on-chain governance would be capped at a maximum of 10%, based only on the tokens it actively chooses to stake. This mechanism is a common design in decentralized networks to prevent excessive influence by any single party. Context and Strategic Rationale for the Shift This proposal did not emerge in a vacuum. It reflects a calculated strategic pivot by both Opera and the Celo Foundation. For Opera, accepting tokens aligns its financial incentives directly with the growth and adoption of the Celo blockchain. As the ecosystem expands and the utility of the CELO token increases, Opera’s treasury benefits proportionally. This creates a powerful feedback loop: Opera has a stronger motivation to drive user adoption through MiniPay, which in turn boosts the ecosystem and the value of its token holdings. For the Celo Foundation, the move conserves cash reserves while potentially securing a more committed and incentivized long-term partner. It transforms Opera from a vendor into a true ally. Industry analysts often refer to this model as “skin in the game,” where partners are economically bonded to the network’s success. This alignment is considered crucial for sustainable ecosystem development, especially in the competitive landscape of layer-1 blockchains. The Role of MiniPay and Opera’s Browser Ecosystem Central to this entire partnership is Opera’s MiniPay wallet . Launched initially in specific African countries, MiniPay is a streamlined, self-custody wallet built directly into the Opera browser. It is designed for low-data environments and focuses primarily on stablecoin transactions, making it an ideal gateway for Celo’s mobile-first, real-world financial applications. Partnership Aspect Old Model (Cash Grants) New Proposal (Token Allocation) Compensation Quarterly USD payments 160M CELO tokens vested over 3 years Opera’s Role Service provider / integrator Major stakeholder & aligned partner Primary Incentive Contractual obligation Direct financial stake in ecosystem growth Governance Influence Likely minimal or advisory Capped at 10% based on staked tokens The success of MiniPay as an onboarding funnel provides tangible value to Celo. By embedding crypto functionality seamlessly into a mainstream web browser used by hundreds of millions, Opera lowers the barrier to entry significantly. The proposed token deal effectively monetizes this strategic distribution advantage for Opera in a way that is pegged to the network’s own growth metrics. Market Implications and Precedents This type of partnership is becoming an increasingly common template in the blockchain industry. Other technology firms have engaged in similar deals, exchanging services, integration, or user access for large allocations of native tokens. These arrangements allow blockchain projects to leverage existing user bases and infrastructure without large upfront capital expenditures. For the technology firms, they represent a strategic diversification into crypto-native assets and revenue streams. The proposal will now enter Celo’s on-chain governance process. CELO token holders will debate and vote on whether to approve the allocation. Key discussion points will likely include the concentration of token ownership, the vesting schedule’s adequacy, and the specific performance expectations from Opera post-allocation. The governance vote serves as a critical check, ensuring the community agrees the long-term benefits outweigh the dilution of the token supply. Conclusion Opera’s proposal to swap cash grants for 160 million CELO tokens represents a profound strategic deepening of its partnership with the Celo ecosystem. This move transitions the relationship from a transactional service agreement to a model of deep economic and operational alignment. By becoming a major stakeholder, Opera signals strong conviction in Celo’s future, while the governance cap seeks to balance this new influence with the network’s decentralized principles. The outcome of the pending governance vote will not only determine the fate of this specific proposal but also signal how mature blockchain networks choose to structure high-stakes partnerships with traditional technology giants. The proposed Opera CELO tokens deal is a landmark case study in the evolving relationship between Web2 and Web3 business models. FAQs Q1: What is Opera proposing to change in its deal with Celo? Opera is proposing to replace its existing quarterly cash grant payments from the Celo Foundation with a one-time allocation of 160 million CELO tokens, which would be distributed to Opera over a three-year period. Q2: How significant is a 160 million CELO token allocation? The allocation is substantial, representing approximately 27% of the current circulating supply of CELO and about 16% of its maximum total supply, instantly making Opera a major stakeholder in the network. Q3: Will Opera control Celo’s governance with this many tokens? No. The proposal includes a specific limitation stating that Opera’s voting power in on-chain governance will be capped at a maximum of 10%, based only on the tokens it actively stakes, not its total allocation. Q4: Why would Opera prefer tokens over cash payments? Accepting tokens aligns Opera’s financial success directly with the growth and adoption of the Celo ecosystem. If the network becomes more valuable and widely used, the value of Opera’s token holdings increases, creating a stronger incentive for it to contribute to that growth. Q5: What happens next with this proposal? The proposal must now go through Celo’s formal on-chain governance process. CELO token holders will discuss, potentially amend, and finally vote to either approve or reject the change to the partnership agreement. This post Opera CELO Tokens: Strategic Pivot Sees Browser Giant Propose 160M Token Stake first appeared on BitcoinWorld .

19 Mar 2026, 13:20

Gold Price Prediction: Fed Slashes Rate Cut Outlook and Sends Gold Crashing 10% From $5,000 — Where Is the Floor?

Gold is in freefall and the chart looks ugly fueling bearish price prediction. After consolidating near all-time highs above $5,000 for most of early 2026, the metal cracked hard. Two consecutive sessions wiped roughly 6%. The $5,000 psychological barrier broke on Wednesday. Thursday extended the drop to $4,500. The trigger was the Fed dot plot. A hold was priced in. What nobody expected was the projection for 2026 rate cuts getting trimmed from two down to one. February PPI came in at plus 0.7%, well above consensus. Markets got caught completely offside. FOMC March SEP: The Fed kept the cuts path unchanged, still showing one 25 bp cut in 2026 and another in 2027. But the new projections leaned a bit more hawkish underneath that. 2026 GDP was revised up to 2.4% from 2.3%, core PCE was raised to 2.7% from 2.5%, and the longer-run… pic.twitter.com/M3g68DGNwo — Wall St Engine (@wallstengine) March 18, 2026 Bond markets reacted immediately. 10-year Treasury yield surged to 4.2%. Dollar Index climbed toward 99.9. That combination is toxic for non-yielding assets like gold. This is not a trend reversal. It is a brutal repricing. The question is no longer how high gold goes. It is where the floor actually is. Gold Price Prediction: Can Gold Hold the $4,500 Level? The break below the 50-day moving average near $4,978 triggered a momentum cascade. Long positions liquidated into a thin order book. Volume confirmed this was a high-conviction bear move, not a shakeout. Gold is now trading near $4,500. Technically oversold but no rejection wick in sight. Bears are still in control. Source: TradingView Lose $4,500 and the next structural floor is $4,350. To even neutralize the immediate bearish thesis, bulls need to reclaim $4,978. That is a long way up from here. The geopolitical backdrop is making it worse. Oil topping $100 is the same force driving inflation higher and forcing the Fed to keep rates elevated for longer. That kills the traditional safe haven argument for gold entirely. Higher rates mean a stronger dollar and a higher opportunity cost for holding a non-yielding asset. Gold is caught in a trap of its own narrative. The very crisis driving people toward it is also the reason the Fed cannot cut rates to make it attractive again. Maxi Doge Targets Early Mover Upside as Gold Liquidity Rotates Gold is bleeding. And capital is looking for somewhere to go. When traditional safe havens crack under hawkish monetary policy, speculative volume does not sit still. It rotates fast into high-beta assets built for exactly this kind of volatile environment. Maxi Doge is catching that flow right now. The presale has raised exactly $4,689,783.01. Current price is $0.0002809. The pitch is unapologetically loud. A 240-lb canine juggernaut built around the 1000x leverage mentality. Holder-only trading competitions, dynamic APY staking, and an ethos that cuts straight to the point. Never skip leg day. Never skip a pump. Gold investors are staring at red candles and questioning the safe haven narrative. Traders chasing variance and ROI are looking at a completely different chart. Maxi Doge is positioning itself as the destination for that rotation. Visit the Official Maxi Doge Website Here The post Gold Price Prediction: Fed Slashes Rate Cut Outlook and Sends Gold Crashing 10% From $5,000 — Where Is the Floor? appeared first on Cryptonews .

19 Mar 2026, 13:19

Crypto stocks plunge as rate cut hopes dampen

More on Bitcoin USD, Ethereum USD Bitcoin Vulnerable: Fed May Signal Higher-For-Longer Bitcoin Morning Strength Bitcoin: The Four-Year Cycle Is A Coincidence, And I'm Adding On The Weakness S&P 500 to be offered as 24/7 crypto-linked contract Bitcoin is back to $71K, what does this mean for the crypto?

19 Mar 2026, 13:16

Ripple Price Prediction: The Good and The Bad for XRP After Failed Rebound

XRP is trying to build a short-term recovery, but the broader trend still leans cautious. The recent bounce has improved momentum on both pairs, yet the price is still trading beneath major trend-defining resistance levels. In other words, sellers are no longer fully in control of the very short term, but buyers have not done enough to claim a real trend reversal either. XRP/USDT Analysis: The Daily Chart On the XRP/USDT chart, the asset has pushed back toward the mid-$1.40s after defending the $1.10 to $1.20 demand zone earlier this month. That rebound matters because it keeps XRP off the lows and lifts RSI back into a healthier range, but the price is still stuck inside the descending structure and below the first major supply band around $1.75 to $1.80. That leaves XRP in a tricky spot. The current move looks constructive, but it still resembles a relief rally inside a larger downtrend rather than a clean breakout. If buyers can force a reclaim of the $1.75 to $1.80 region, the door opens toward the much heavier $2.40 to $2.50 resistance area. But the price would also need to climb above both the 100-day and 200-day moving averages to reach this area. Until then, the bounce is not decisive. XRP/BTC 4-Hour Chart The XRP/BTC pair is telling a similar story. After repeatedly holding the 2,000 sats area, XRP has started to recover a bit and is now pressing back above that support zone. Momentum has improved, and the pair no longer looks as weak as it did during the recent dip, though it is still trading under both the 100-day and 200-day moving averages. For the BTC pair, the first task is to turn this rebound into follow-through. A push through the 2,100 to 2,200 sats area would be a good start, and lead to a breakout above both key moving averages. But the real test remains higher at 2,400 to 2,500 sats, where layered resistance and the broader downtrend line converge. If XRP gets rejected before that, the market likely falls back into the same sideways-to-bearish range. However, if it breaks through, the tone shifts from simple stabilization to genuine recovery. The post Ripple Price Prediction: The Good and The Bad for XRP After Failed Rebound appeared first on CryptoPotato .

19 Mar 2026, 13:16

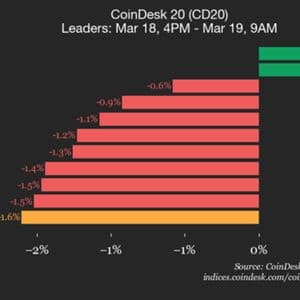

CoinDesk 20 performance update: NEAR Protocol (NEAR) drops 3.3%, leading index lower

Hedera (HBAR), down 2.9% from Wednesday, was also an underperformer.